When researching successful dynamic pricing strategies, most case studies fall into one of two camps. One reads like a vendor brochure: uplift numbers from unnamed companies, with no denominator and no measurement method. The other is the cautionary tale: Wendy’s, Uber surge pricing, Coca-Cola’s hot-day vending-machine idea, then the implied lesson that dynamic pricing is too risky to fund.

Neither helps a CFO decide whether to back a dynamic pricing program next quarter.

We’ve spent the last several years watching pricing programs succeed and fail across pharma, B2B distribution, storage technology, and consumer goods. The pattern is consistent: the algorithm rarely separates the wins from the headlines. The operating model does. Fences, override authority, measurement, kill switches, and the executive narrative decide whether the math survives contact with customers, sales, and finance.

According to Revology’s research of 2,000 global companies, a 1% improvement in price realization produces a 6–7% lift in operating profit. In unregulated industries, this figure is in the 10–11% range. That is the economic reason to care. If a dynamic pricing program cannot demonstrate clear price movement in realized prices, it is not yet a P&L program.

Table of Contents

- Dynamic pricing case studies — what “success” actually looks like

- Case study cluster 1 — retailers that got dynamic pricing right

- Case study cluster 2 — when dynamic pricing fails publicly

- Case study cluster 3 — B2B and capital-equipment dynamic pricing

- A practical operating model — 6 steps that separate winners from headlines

- KPIs and the executive scorecard

- Frequently asked questions about dynamic pricing case studies.

- How to evaluate a dynamic pricing vendor or build versus buy

- Conclusion and next steps

Dynamic pricing case studies — what “success” actually looks like

Two ways dynamic pricing programs end up. Value-aligned execution adds margin quietly. Punitive optics trigger backlash. The difference is rarely the math.

Dynamic pricing case studies are useful only when they show three things: the economic result, the measurement method, and the operating constraints around the model. Programs that quietly add margin usually do it by segmenting demand and setting fences. Programs that fail publicly usually lack fairness, disclosure, or a kill switch. B2B implementations often look less dramatic than retail examples, but the discipline can be sharper because every recommendation has to survive sales negotiation and finance review.

When evaluating a dynamic pricing program, we use six lenses to determine its success: revenue, margin, share, brand trust, leakage, and time-to-impact. Revenue without margin is noise. Margin without a share context can be dangerous. A 4% margin lift that comes with 200 basis points of share loss may be a bad trade. The lens matters.

Case study cluster 1 — retailers that got dynamic pricing right

The retail wins we know best share a pattern: they let the algorithm move price, but only inside fences set by a human pricing committee. Some examples follow. Two are anonymized client engagements; one is public.

The retail pattern that works: invisible price flex on perishables and high-velocity inventory, governed by electronic shelf labels and a central data spine. The mechanics stay below the customer’s perception threshold; the margin continues to compound.

A global e-commerce platform — 4.2% margin lift via promotional guardrails

The algorithm was doing exactly what it had been asked to do. It was told to cut the price until it won the buy box. The missing instruction was margin discipline. On hero SKUs, where willingness to pay was well above the competitive floor, the engine was giving away economics that customers were not demanding.

We added three fences: an 8% movement cap in any 24-hour window, a tighter 4% markdown limit on the hero-SKU list, and a pause rule after five price moves in a week. That last rule mattered more than it looked. It forced a buyer to sanity-check whether the engine was responding to real competitive pressure or chasing noise.

A specialty grocer — 21% waste reduction on perishables clearance

Specialty grocers have a particular problem with perishables. A box of strawberries that doesn’t sell by Friday becomes waste by Sunday, and the marginal cost of clearing it is essentially the foregone full-price margin from earlier in the week. A dynamic markdown engine should be obvious.

In practice, most grocers operate static markdown ladders — 25% off on day three, 50% off on day five, donate or discard on day six. The ladder rarely accounts for category-specific shelf life, weather, or store-level traffic patterns.

A regional specialty grocer (anonymized client) replaced its static ladders with a dynamic markdown engine that scored each unit on a freshness model, weather-adjusted demand expectation, and

store-level historical clear-through rates. The engine outputs a recommended markdown by 6 a.m. each morning, which the store manager could accept or override.

Year one outcome on the perishables categories: 21% reduction in waste tonnage, 1.8% gain in category margin. The reduction in waste was the headline because the grocer also reported it in its sustainability disclosures. The margin gain was what funded the next year of the program.

A Fortune 500 mass retailer — competitive-response engine without race-to-the-bottom

This one is public, drawn from analyst coverage and the company’s own investor commentary. A large U.S. mass retailer rolled out a competitive-response pricing engine in 2024, tied to real-time scraping of three named competitors. The engine matches a competitor’s price within fences: a minimum-margin floor on every SKU and an absolute price cap below which no item can be set, even if a competitor goes lower.

The retailer reported a 1.5–2.0% margin improvement on the watched assortment in the first four quarters. Analyst commentary notes that the program quietly avoided the race-to-the-bottom failure mode that earlier matching engines triggered at other chains, because the floor was non-negotiable. The engine could match — but only down to a hard limit.

The common thread across all three retail wins: the algorithm is fenced. Where the human authority sits — promotional desk, category manager, pricing committee — gets to override, and frequently does.

Case study cluster 2 — when dynamic pricing fails publicly

The press loves dynamic pricing failures because they fit neatly into a “tech overreach” narrative. The actual failure mode is almost always disclosure and fairness, not the algorithm.

The capability-first announcement that became a brand crisis. The technology was unremarkable. The framing — “dynamic pricing” read as “surge pricing” — produced millions of negative impressions before the program ever shipped.

The Wendy’s 2024 surge-pricing announcement

In early 2024, Wendy’s announced it would test “dynamic pricing” on digital menu boards. The news cycle reacted within hours, the company walked the announcement back within days, and the term “surge pricing” became a brand-trust liability that Wendy’s spent the rest of the year managing.

The technical problem was small. Wendy’s was actually piloting digital menu boards that could change prices at certain times of day — a tactic that grocery stores and quick-service operators have used for decades through paper menu rotations. Wendy’s framed it as “dynamic pricing,” which the public reads as “surge.”

Two things went wrong. The announcement framed the program in terms that triggered the surge-pricing memory (Uber, ride-share, peak pricing). And the company didn’t pre-position with customer research, franchisee briefings, or a public fairness commitment. A pilot that would have been unremarkable became a brand crisis because of how it was named and announced.

There’s a lesson in the symmetry: the algorithm is not what fails. The communications strategy fails first.

Coca-Cola vending machines, 1999 — the original cautionary tale

In 1999, Coca-Cola’s then-CEO floated the idea of vending machines that would raise prices on hot days. The internal logic was straightforward — willingness to pay for a cold soda is higher in 95-degree heat than in 60-degree weather. The external reaction was severe enough that the company never deployed the technology.

What’s instructive 25 years later is that the technology is now trivially available. Connected vending machines, weather APIs, and real-time inventory levels — none of this is hard. What kept Coca-Cola from deploying it in 1999 wasn’t the engineering. It was the fairness signal: the same customer paying more on a hot day reads as exploitation.

The fairness signal hasn’t changed. If anything, social media makes it sharper. Programs that don’t think hard about fairness — and don’t pre-position the fairness story — get crushed by it.

Uber surge pricing and the disclosure trade-off

Uber surge pricing is the dynamic-pricing case study most consumers have personal experience with, which makes it a useful teaching case even though Uber’s outcome is mixed. The company’s surge mechanism is mathematically sophisticated and economically defensible. The complaint isn’t really about the surge math. It’s about the disclosure context.

Surge pricing has been most controversial in moments where customers had limited alternatives — Hurricane Sandy, the Sydney café siege, and New Year’s Eve in cities where transit had shut down. The mechanism that nudges supply toward demand also produces price points that look exploitative when alternatives evaporate. Uber’s response over the years has been to add caps during declared emergencies, surface the multiplier more clearly, and — eventually — replace the multiplier display with an absolute dollar price.

The lesson isn’t that surge pricing is wrong. It’s that disclosure design has to anticipate the moments when the price will look exploitative, even when the math is fine.

Case study cluster 3 — B2B and capital-equipment dynamic pricing

The B2B dynamic-pricing story rarely makes the press because it isn’t theatrical. Quarterly negotiated contracts moving up 2.5% instead of 1.5% doesn’t trend. But the dollar volumes are large, and the discipline is sharper than the retail discourse suggests.

Dynamic pricing in industrial distribution. Predictive supply-chain analytics drive price moves that customers accept because the pricing flex is paired with availability and reliability — value the buyer can see.

A global pharmaceutical manufacturer — above-inflation pricing with share gain

We worked with a global pharma manufacturer (anonymized) operating across emerging markets. The traditional pricing model in the company’s affiliate countries was annual list-price increases tied roughly to local inflation, with country-by-country negotiation depth.

We helped restructure the pricing into a more dynamic framework. Country teams now receive quarterly recommended price-change windows from a central pricing model that accounts for local inflation, currency movements, competitor activity in the same molecule class, and patient affordability signals from the previous quarter’s volume data. The recommendations are advisory — country leadership still owns the price decision — but the central recommendation creates a baseline.

The result over four quarters was net price realization 180 basis points above the prior year, with no observed market share loss in the affected molecule classes. The share point matters: this was not price taking, offsetting volume loss. It was price taking with volume held.

The above-inflation outcome ran counter to the standard pharma narrative that dynamic pricing is impossible in regulated markets. The frame was different: the company didn’t try to outrun regulation; it adjusted prices inside regulated bands, country by country.

A storage-technology OEM — long-cycle B2B price realization

A storage-technology OEM (anonymized client) sells primarily through long-cycle B2B contracts — six- to nine-month negotiation cycles with hyperscale and enterprise customers. The list price is a starting point; the realized price reflects deal-by-deal negotiation, volume tiers, multi-year commitments, and competitive context.

The pre-existing model was deal-desk-centric. Sales engineers proposed configurations, the deal desk priced them, and a margin floor was enforced at the line-item level. The challenge was that the line-item floor produced predictable patterns competitors had learned to exploit: discount stacking on attached storage, accessory packs, and services to bring the blended margin within tolerance.

The dynamic component the company added was a deal-level — not line-item-level — margin model that updated with every quarter’s win/loss data. The model produced a “willingness to walk” envelope for each deal class: above the upper bound, sales should hold firm; below the lower bound, the deal probably wasn’t worth winning.

An industrial PE-backed distributor — dynamic guardrails at the channel

An industrial distributor (anonymized, PE-backed) was running a single national list price with branch-level discounting authority. The branches in low-competition regions were discounting at roughly the same depth as branches in high-competition regions, because the discount authority limits were uniform.

The change was simple in concept but difficult to execute: we built a competitive-density score for each ZIP code, which translated into a branch-specific discount authority level. Branches in low-density regions could still discount, but the maximum discount before requiring regional sign-off dropped by 4–6 percentage points. Branches in high-density regions saw their authority expand modestly, giving them greater flexibility against local competitors.

The hard part was rolling it out without telling branch managers that some of them had been over-discounting for years. The communication was framed as “dynamic guardrails” — the system adapts to local competitive conditions, and the limits adapt with it.

Year one outcome on the watched product families: blended gross margin up 110 basis points, with branch-manager retention unaffected. The framing carried the program.

A practical operating model — 6 steps that separate winners from headlines

Across the cases that worked, six elements were present. In the failed cases, at least one was missing. The operating model is not a bureaucracy around the algorithm. It is the part of the system that tells the algorithm what risks the company is willing to take.

The six-step operating model. Each step closes a failure mode we’ve seen break dynamic pricing programs in the wild. Skipping any one of them is how programs end up in the press for the wrong reasons.

Step 1 — Segment demand by customer, product, channel, and timing

The first failure mode is treating all demand as the same demand. A day-two perishable and a day-five perishable are not the same product. A low-competition branch and a high-competition branch should not have the same discount authority. A renewal negotiation and an expansion motion should not use the same walk-away logic. In practice, four to eight demand segments per category are usually enough. Fewer losses in precision; more creates operational drag, and the field will not follow.

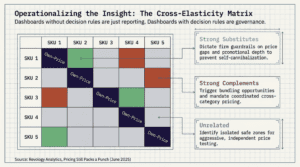

Step 2 — Set price fences, fairness rules, and disclosure choices

Fences are where the e-commerce example recovered margin. The engine knew how to win the buy box, but it lacked a hero-SKU cap, a movement limit, and a pause rule after repeated price moves. Each segment needs a floor, a ceiling, and a movement-velocity cap. Fairness rules sit above those fences: no emergency-period increases on essential items, no hidden customer-by-customer price spread inside the

same channel, and no model behavior, the company would be unwilling to explain publicly. Disclosure choices decide whether customers see the mechanism or only the outcome.

Step 3 — Build the data and measurement spine

Most failed programs have usable data feeds but weak attribution models. That is when the CFO asks what pricing added this quarter, and the answer comes back as, “Revenue is up, but we cannot isolate the pricing effect.” The measurement spine needs three layers: the data feed, the attribution model, and the executive dashboard. According to Revology’s research of 2,000 global companies, a 1% improvement in price realization produces a 6–7% lift in operating profit. In unregulated industries, this figure is in the 10–11% range. That math only matters if price realization is measured cleanly.

Step 4 — Govern with a pricing review cadence and clear authority levels

Without a cadence, the e-commerce engine keeps cutting until margins erode, the distributor branch network keeps discounting when competition is light, and the CFO override happens live rather than through a structured escalation. The cadence should be weekly tactical, monthly portfolio, quarterly strategic, and annual architecture reset. The pricing engine has authority inside fences. The pricing committee owns fence parameters. Finance owns material P&L risk. Executive leadership owns fairness and public narrative choices.

Step 5 — Pilot, monitor, scale, and define the kill switch

Every pilot needs a kill switch before launch. The trigger might be a complaint rate, a watched-segment share-loss, a regulatory inquiry, a media-sentiment threshold, or a CFO-defined margin-floor breach. The point is to stop quietly on a defined signal rather than stop publicly after trust has already been damaged. Wendy’s showed how quickly a small pilot can become a brand story when the signal is not closely monitored.

Step 6 — Build the executive-grade narrative before the press does

The company needs its own explanation before someone else writes one. Wendy’s did not have a customer-friendly framing of the menu board change before the press labeled it “surge pricing.” Coca-Cola did not have a fairness commitment ready before the hot-day vending-machine story hit. Uber took years to make emergency-period caps and price disclosure feel like part of the system rather than a concession. The narrative should explain why the program exists, who benefits, what the fences are, what the fairness rules are, and when the company will pause.

KPIs and the executive scorecard

The four-quadrant executive scorecard. Finance, operations, sales, and brand all see the same review. A committee that watches only the margin will miss the trust signal until it has already gone public.

The executive scorecard should separate economic impact, adoption, customer trust, and risk. Price realization versus list is the headline metric, but it cannot stand alone. Margin lift attributable to pricing should isolate mix, volume, and seasonality. Discount leakage should show the dollars given away outside the policy. Rule coverage should show the share of transactions that now pass through the dynamic logic, while the override rate should show whether the field trusts the recommendations. If rule coverage sits below 70% after the pilot period, legacy pricing still owns the business. If the override rate sits above 30%, either the fences are wrong, or the rollout has not earned field adoption.

Customer and risk signals need the same discipline. Complaints per 100,000 transactions should be baselined before launch. Retention or Net Promoter Score should be tracked in the affected segments, not across the full customer base, where the signal gets diluted. Distance to kill-switch triggers should be a standing agenda item in the pricing review. A committee that sees only the margin will miss the trust signal until it becomes public.

Frequently asked questions about dynamic pricing case studies.

What’s the difference between dynamic pricing and surge pricing?

Surge pricing is one branch of dynamic pricing. It responds to short-term demand spikes, usually in near real time. Dynamic pricing also includes markdown engines for perishables, competitive-response rules for retail, B2B contract-pricing envelopes, and personalized offer construction. The governance question changes by use case: surge pricing needs disclosure and emergency caps; B2B dynamic pricing needs authority rules, deal-level margin logic, and clean win/loss feedback.

Do B2B companies use dynamic pricing, or is it just retail?

B2B companies use dynamic pricing, but the cadence is slower, and customer signals differ. A distributor adjusting branch discount authority by local competitive density is using dynamic pricing. A storage OEM updating deal-level walk-away thresholds from quarterly win/loss data is using dynamic pricing. The recommendation may be updated monthly or quarterly rather than minute by minute, but the mechanism is the same: current data informs a price move, and humans decide within their fences.

How do you measure ROI on a dynamic pricing program?

Measure ROI by isolating price realization from volume, mix, and seasonality, then comparing the dynamic-pricing arm against a control or holdout segment. According to Revology’s research of 2,000 global companies, a 1% improvement in price realization produces a 6–7% lift in operating profit. In unregulated industries, this figure is in the 10–11% range. Without a counterfactual, the team ends up debating whether the lift came from pricing, demand, or product mix.

What’s the most common reason dynamic pricing fails publicly?

Dynamic pricing usually fails in public before it fails in the model. Wendy’s, Coca-Cola’s hot-day vending-machine idea, and Uber’s emergency-period surge backlash all point to the same operating gap: the fairness story was weak or late. Customers can accept price variation when the reason is clear and the boundaries are visible. They push back when the mechanism feels hidden, opportunistic, or disconnected from a service benefit.

How long until a dynamic pricing program shows revenue impact?

Retail programs can show a measurable margin effect within three to six months when the data feed, attribution model, and operational approval path are ready at launch. B2B contract programs usually take six to twelve months because renewals, negotiations, and volume commitments roll through slower cycles. First-quarter promises are credible only when the program is recapturing obvious leakage, such as unmanaged discounting or stale markdown ladders.

How to evaluate a dynamic pricing vendor or build versus buy

Most enterprises end up with a hybrid: a commercial pricing platform handles the heavy lifting of segmentation, rule execution, and scale, while an internal analytics team owns the attribution model, segmentation strategy, and executive dashboard.

Build path

The build path makes sense when:

- Your data feeds are unusual (industry-specific signals that vendor models don’t ingest).

- Your fairness rules are highly specific (regulated industries, customer-promise commitments).

- You have an existing analytics team with experience in elasticity modeling, attribution, or Bayesian inference.

The build path has lower software cost and higher people cost. Expect 6–9 months to a first usable version.

Buy path

The buy path makes sense when:

- Your category is well served by an existing vendor (retail, SaaS, and hospitality have many options).

- You need the program to live in a quarter, not a year.

- The vendor’s data feeds and rule library cover most of your use cases out of the box.

What to test in a vendor POC: the attribution model (not just the rule engine), the override workflow, the explainability of recommendations (can a category manager understand why the engine recommended a change?), and the data export (can you pull recommendations and outcomes back into your own analytics stack?).

Hybrid path

The hybrid path is what most enterprise programs actually look like. A commercial pricing platform handles segmentation, rule execution, workflow, and high transaction volume. The internal analytics team owns attribution, segmentation strategy, governance, and the executive dashboard. The vendor’s role is the engine. The company’s role is the operating model.

In a vendor proof-of-concept, start with the attribution model rather than the rule engine. Test whether a category manager can understand the recommendation, whether the override workflow captures reason codes cleanly, whether outcomes can be exported into your analytics stack, and whether the model can explain price realization movement after mix and volume are isolated.

The mistake is treating the vendor as a complete solution. The cases that fail publicly almost always have a vendor underneath. The vendor isn’t the problem — the absence of a coherent in-house operating model around the vendor is.

Conclusion and next steps

The dynamic pricing case studies that work share operating discipline: fences, fairness rules, measurement, a kill switch, and a narrative the company can defend. The failures usually miss one of those pieces. If you are considering a dynamic pricing program, or if one is already running and the operating model feels incomplete, Revology’s diagnostic benchmarks the six steps and identifies the highest-return next move.

Book a pricing & revenue management diagnostic call at revologyanalytics.com/contact-us. The first call is a conversation, not a sales pitch — we’ll tell you where your program sits relative to the operating model and where the highest-leverage next step is.